If you want to attain financial freedom, you must embrace the practice of budgeting. This article is an in-depth guide to budgeting for individuals and organizations in 2024. Learn all you need to know about budgeting here!

First, What is a Budget?

A budget is a financial plan for your income, expenses and savings over a specific period, typically monthly. In a budget, you allocate your resources to your expense categories such as housing, transportation, feeding, and savings.

Second, What is Budgeting?

Budgeting, therefore, is the strategic allocation of your resources to cover your expenses and savings over a specific period, typically monthly. It is a proactive step towards expense tracking, consistent savings and financial freedom.

Why Do You Need to Create a Budget?

Here are some important reasons why you should take the time to create a budget, even if it seems like a chore.

- Financial Awareness: Sometimes, your income looks like a whole lot, until you sit down to allocate your resources. A budget gives you a clear picture of what you earn, what you spend it on, how much you should spend and what you should save. In a budget, your expenses are categorized such that you can see what is taking a chunk of your resources and where you can cut back.

- Wise Spending: Have you ever been paid your salary at the end of the month only to spend it all in a week? This should not happen, under normal circumstances! A budget allows you to allocate your resources towards your expenses, debts and savings over a period, usually monthly. With a budget, you can identify when you are going overboard with your expenses.

- Debt Management: A budget helps you to be more financially responsible towards those you owe. In a budget, you can allocate consistent contributions towards repaying your debts within a stipulated timeframe. You can also determine when to repay more or less.

- Consistent Savings: Saving a specific percentage of your income every month is a life-changing hack. Budgeting helps you to save consistently towards your financial goals. It also helps you to build an emergency fund for the rainy days.

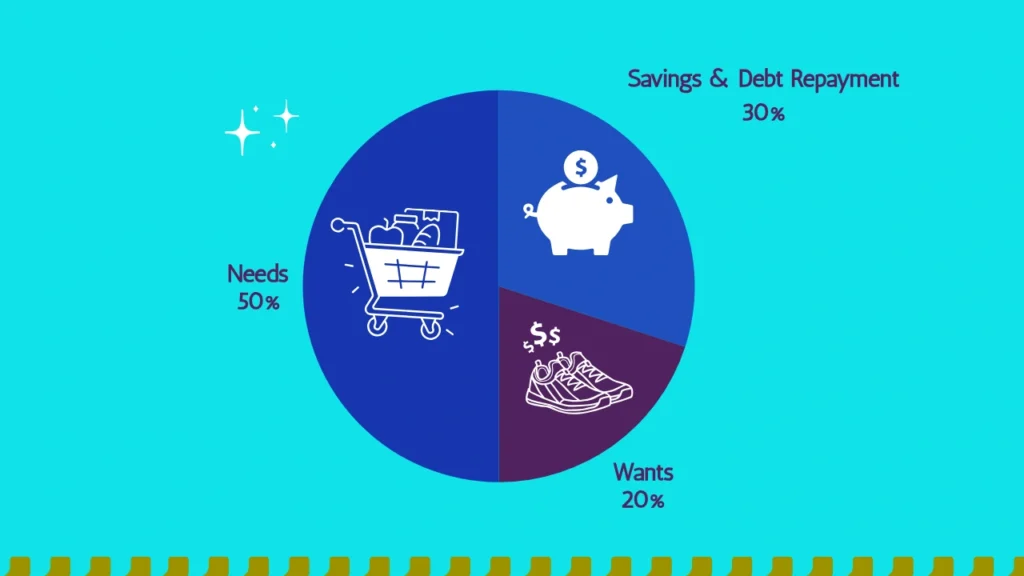

The 50/30/20 Rule

Imagine your income as a mouth-watering cake that consists of three flavors: red velvet, chocolate, and vanilla. Let’s say you absolutely love the red velvet flavor, so it makes up half of your cake.

The chocolate flavor is your next favorite, so it makes up 30% of your cake. Vanilla is not your favorite, but your mother likes it. So, to make her happy, one-fifth of your cake is vanilla flavor.

When your cake arrives, you cut it into neat portions, each with its respective flavor, to enjoy every bite to the fullest. The red velvet flavor portion of your cake represents 50% of your income.

The chocolate flavor portion of your cake represents 30% of your income. Finally, the vanilla flavor portion of your cake represents 20% of your income. This cake analogy represents the 50/30/20 rule.

The 50/30/20 rule, also known as the “balanced money formula,” suggests allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayments. It is suitable for beginners in budgeting, as well as people who do not have a lot of debts to repay.

The 50/30/20 rule is often attributed to Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, who elucidated the rule in their book, “All Your Worth: The Ultimate Lifetime Money Plan.” However, it is worth noting that while they popularized this rule, its principles have been advocated by various financial experts before their book was published.

Brief Digression into Other Budgeting Rules

You may not be familiar with other budgeting rules. Here is a quick rundown of a few other budgeting rules besides the 50/30/20 rule.

- Envelope System: This is a cash-based budgeting method where you allocate a certain amount of cash to different categories, such as groceries, entertainment, transportation, and place each amount in separate envelopes. Once an envelope is empty, you stop spending in that category for the month. It’s a tangible way to stick to your budget and avoid overspending. This strategy is appropriate for those who earn in cash or need a tangible system to curtail their spending.

- Percentage-Based Budgeting: Similar to the 50/30/20 rule, this method involves allocating percentages of your income to different categories, but the ratios may vary based on your priorities and financial goals. For example, you might allocate 25% to housing, 15% to transportation, 10% to savings, and so on. This strategy is appropriate for individuals who have the freedom to distribute resources properly without being hampered till their next paycheck.

- Zero-Based Budgeting: In this method, every dollar of your income is assigned a specific purpose, such as expenses, savings, or debt repayment. The goal is to “zero out” your budget so that your income minus your expenses equals zero. It requires meticulous tracking and planning but can be very effective in controlling spending and maximizing savings. The zero-based budgeting method is appropriate for those who can precisely estimate, plan and track their expenses and savings throughout the month.

- Pay Yourself First: This strategy involves prioritizing savings by setting aside a portion of your income as soon as you receive it, before paying any bills or expenses. This ensures that savings become a non-negotiable part of your budget and helps you build wealth over time. This strategy is appropriate for individuals who have the freedom to distribute resources properly without being hampered till their next paycheck. This technique is excellent for folks who want their savings to be an inevitable part of their budget. Many people who use this technique automate their savings using budgeting apps.

- Bi-Weekly Budgeting: Instead of budgeting on a monthly basis, some people prefer to manage their finances based on their bi-weekly paychecks. This makes it easier to track their expenses. This is suitable for business owners or workers who earn on a daily or weekly basis.

How to Budget Money Using the 50/30/20 Rule

Alright, let us go back into the crux of this section. We’re going to take a closer look at the 50/30/20 rule and really break down how to allocate your resources.

50% Allocation to Needs

“Needs” refer to the essential requirements for day-to-day survival, such as air, water, food, sleep, clothing, shelter, income, and so on.

According to Maslow’s hierarchy of needs, people must first satisfy their basic physiological needs, such as food, clothing, and shelter, before they can fulfill their self-actualization needs, such as morality, purpose, and acceptance. This is largely true because only a person who is physically healthy can resist the immoral temptation of theft or seek to fulfill destiny.

Needs vary from person to person, based on various factors, such as age, location, and health status. For instance, a pregnant woman may require monthly hospital visits as a necessity, while a healthy man in his prime may not need to visit a hospital for months.

The 50/30/20 rule recommends that half of your income after taxes should cover your monthly needs. If 50% of your income cannot meet your needs, it may be a sign that your current phase of life requires more money than you are making.

30% Allocation to Wants

“Wants” refer to the things we desire or crave but do not need for survival. They are the extras, the cherry on top of life’s sundae. Wants to encompass a wide range of goods, services, experiences, and indulgences that bring us pleasure, entertainment, or convenience.

These can include dining out at fancy restaurants, splurging on designer clothes, treating ourselves to luxurious vacations, or enjoying entertainment like movies or video games. Wants to enhance our quality of life and make it more enjoyable, but they’re not essential for our survival or well-being.

Although wants may appear to be lavish expenses, they can actually overlap with your needs category by including any desired upgrades to your basic necessities. However, the 50/30/20 rule suggests that these upgrades remain within the confines of 30% of your income.

For example, a black lady doctor may need to purchase a “work-wig” because she cannot make time to constantly manipulate her hair into pretty weaves. She may upgrade her need by planning to buy a 10” Vietnam raw donor bone straight wig, instead of a 10” China human hair blend wig.

However, if this 10” Vietnam raw donor bone straight wig is 5 times her 30% allocation for wants, she may need to purchase the China 10” human hair blend wig instead or pay in installments for a 10” Vietnam raw donor bone straight wig.

20% Allocation to Savings & Debt Repayment

Savings are like a financial safety net, a stash of money that you set aside for the future. It is the portion of your income that you don’t spend right away but keep aside for emergencies, big purchases, or long-term goals.

Savings can come in different forms, like putting money into a savings account, investing in stocks or bonds, or contributing to a retirement fund. Whether it’s for unexpected expenses, a dream vacation, or building a nest egg for the future, savings give you peace of mind and financial security.

Saving is also important for debt repayment. It would be inconsiderate to lavish money on your wants, such as a 10” Vietnam raw donor bone straight wig, yet ignore the repayment of a business loan you took from LAPO Microfinance Bank.

Anyone who earns should save. Even children should be taught to save, so they do not grow to be irresponsible adults.

Debts are financial responsibilities stemming from borrowing money, such as student loans, car loans or mortgages. It is only responsible to allocate a reasonable amount towards repaying your debts within the timeframe specified.

The 50/30/20 rule teaches you to save 20% of your income to secure your financial future and repay your debts.

Hypothetical Application of the 50/30/20 Rule

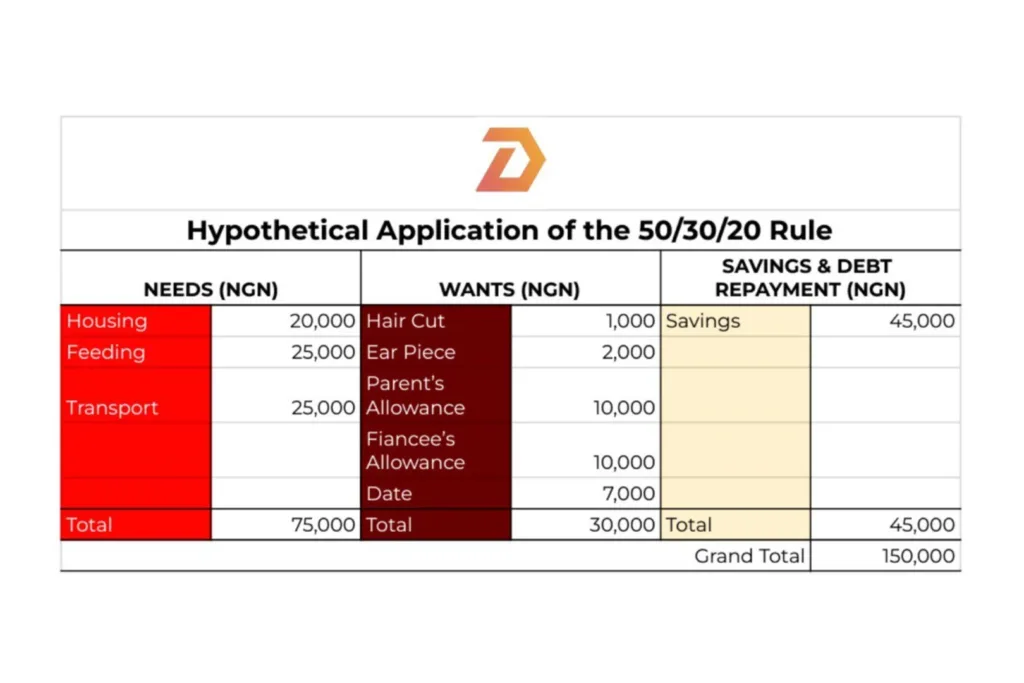

Suppose you are a young Muslim guy who earns 150,000 Nigerian Naira (NGN) per month. Well, this is not a lot of money in relation to the United States Dollar, but Master’s Degree Holders in Nigeria earn this, so let’s work with it.

Dividing your income according to the 50/30/20 rule, we have the following:

- 50% of your income is 75,000 NGN.

- 30% of your income is 45,000 NGN.

- 20% of your income is 30,000 NGN.

Your needs are:

- Housing: 20,000 NGN

- Transportation: 25,000 NGN

- Feeding: 25,000 NGN

- Total: 75,000 NGN

This makes up exactly 50% of your income. However, if your needs slightly exceed 75,000 NGN, it would be reasonable as the 50/30/20 rule is not cast in stone.

Your wants are:

- A clean haircut: 1,000 NGN

- A fake Apple earpiece: 2,000 NGN

- Parent’s allowance: 10,000 NGN

- Fiancée’s allowance: 10,000 NGN

- Restaurant Date: 7,000 NGN

- Total: 30,000 NGN

This makes 20% of your income, as opposed to 30%. As a wise chap, you can save the extra 10% for unforeseen circumstances in Nigeria.

Your savings:

- Savings account: N45,000

This makes 20% of your income, as opposed to 30%, which is applaudable.

Pros of the 50/30/20 Rule

Here are some perks of following the 50/30/20 rule:

- Simplified Budgeting: The 50/30/20 rule is a user-friendly way of budgeting that is easy to comprehend, making it ideal for beginners.

- Spending Flexibility: It allows you to have some flexibility in spending by differentiating between needs and wants, so you can enjoy spending on things you love without feeling too restricted.

- Focus on Savings: By setting aside 20% of your income for savings and/or debt repayment, this rule promotes financial responsibility and encourages you to develop a habit of saving over time.

- Debt Reduction: Prioritizing a portion of your income towards debt repayment can speed up your journey to becoming debt-free, providing financial freedom in the long run.

Cons of the 50/30/20 Rule

The 50/30/20 rule is a popular budgeting method, but it may not be suitable for everyone’s financial situation and goals. Here are three cons of this rule:

- Not One Size Fits All: The 50/30/20 rule is a general framework, and it may not work for people with high living expenses or significant debt.

- Limited Focus on Important Financial Goals: The rule does not consider other vital financial goals such as retirement savings, emergency funds, or investing, which may require more than the allocated 20% for savings.

- Limited Focus on Long-Term Wealth Building: While the rule promotes saving, it may not emphasize investing for long-term wealth accumulation, which is crucial for achieving financial independence and retirement security.

What is the Best Way to Create a Budget?

Maybe the 50/30/20 rule does not apply to you, because you have some financial obligations that exceed the 20% saving and debt repayment allocation. Maybe other conventional methods apply once in a while, but are just unsuitable at other times. You may also just be aloof as to how to actually create a budget that works for you.

I would not be so unkind to create a budgeting guide without sharing practical steps to budgeting. Listed are the steps that are necessary for creating a budget that aligns with your lifestyle and financial goals.

Step 1: Know Your Financial State

The first step to creating a budget that works for you is gaining an accurate perspective of your current financial state.

One, you need to know your estimated net income after statutory deductions and taxes. What do you earn? Do you have an allowance? Do you get bonuses or cash prizes? Is there an asset you recently monetized? Calculate your total income.

Two, think about your routine expenses. How much do you spend on housing, feeding, transportation, airtime, and so on? Look through your bank statement to determine what really takes a chunk of your money. By doing so, you will realize areas that you can cut back on and save money.

Step 2: Set SMART Financial Goals

If you were a second-year undergraduate with a monthly allowance of $250 and a part-time job at a restaurant earning an average of $500 per month, your average income would be $750. There is only so much you can accomplish with $750 per month, so your financial goals must be SMART, or you could live a poor quality of life.

Whether you want to save to purchase a house, pay off debt, or build an emergency fund, defining your financial goals will help you focus your budgeting efforts. You’ll be able to figure out what you need to give up to achieve financial freedom. What are your short, medium, and long-term financial goals?

Step 3: Choose a Budgeting Method

People use a variety of budgeting methods these days, depending on their financial responsibilities and preferences. For example, the 50/30/20 rule is appropriate for budgeting novices with few financial commitments or debts to repay. Consider your phase of life, financial responsibilities and preferences when choosing a budgeting method. If unsure, you could try different approaches until you find the one that suits you and supports your financial goals.

Step 4: Allocate Your Income Wisely

According to your budgeting method, allocate your resources to your needs, wants, debts and savings.

Step 5: Track Your Expenses

Using either an expense tracker or Google Sheets, document all your:

- Net Income: Calculate your income after statutory deductions and taxes. We don’t want any problems with the government, do we?

- Expense Categories: Think about your routine expenses. Your expenses fall into two classes: fixed expenses and variable expenses. Fixed expenses are expenses that you typically spend the same or similar amount of money to cover monthly, such as housing, subscriptions, student loans, and so on. On the other hand, variable expenses are expenses that you spend variable amounts of money to cover monthly, such as feeding, clothing, entertainment, and so on. List your fixed expenses and allocate resources to them. You may look through your bank statements and receipts to get an accurate estimate of the amount you need to budget for every expense. Next, list your variable expenses and allocate resources to them. It is also important that you do not allocate too much money per expense, so as not to overspend. If I were you, I would also create a category for miscellaneous or unexpected expenses.

- Actual Expenses: As the month progresses, record your actual expenses using a budgeting app, expense tracker, spreadsheet or pen and paper. If you are using a spreadsheet or pen and paper, it is best to write what you spend just after you spend it to avoid forgetting or mixing things up. Some free expense trackers and budgeting tools allow you to sync your financial accounts, capture images of receipts, and also manually enter your transactions, so you can track your expenses in one place. Some even send notifications when you overspend. Great, isn’t it? You should try one. I’ll share some free ones as you read this article.

- Estimated Expenses: Document the estimated cost of each category of expense that you have projected. You can check through your receipts or bank statements for a clearer picture of your spending habits per category. Compare your total income to the total of your expenses. Your expenses should not exceed your income. You should also have some money to save. If you notice that your expenses are above or slightly below your income, you may need to cut back on your expenses. A tip for cutting back on your expenses is categorizing your expenses into needs and wants. You should prioritize your needs, such as feeding and housing, above your wants, such as an unnecessary phone upgrade or a new toy.

Step 6: Review Your Budgeting Method

Because life is full of twists and turns, what worked for you last month might not work for you this month. Every month, review and adjust your budgeting method to meet your financial goals. Identify areas where you need to be more financially responsible.

How to Make a Budget Using Google Sheets

Making a budget can be a daunting task especially if you are using pen and paper. Google Sheets is an online spreadsheet by Google used for creating, editing, and collaborating on spreadsheets online. Unlike the traditional Microsoft Excel, which has to be used by a single user per time, Google Sheets can be used via the Internet by multiple users at a time.

Just like Microsoft Excel, Google Sheets can be used to create automated tables and charts using common mathematical formulas. This feature is very useful, particularly in making budgets, which typically require lots of basic mathematics.

This section provides a step-by-step guide on making a budget using Google Sheets. It is friendly for “dummies.” Let’s plunge in!

Two Methods of Making a Budget Using Google Sheets

There are two primary methods for making a budget using Google Sheets:

- Making a Budget Without a Google Sheets Budget Template: You could make a budget from scratch and tailor it to your personal needs while still including the fundamental aspects of a budget, such as income and expenses.

- Making a Budget With a Google Sheets Budget Template: You could make a budget by using a Google Sheets budget template, such as the Monthly Budget Template or the Annual Budget Template. You simply need to edit the placeholder values in the template for your own use.

Making a Budget Without a Google Sheets Budget Template

If you choose to make a budget on Google Sheets from scratch, here are some important steps to take:

Step 1: Setup Your Spreadsheet

- In the case that you have not, download the Google Sheets application from Google Play or App Store.

- Launch Google Sheets and sign up using your email address and password. If you have already signed up, sign in instead.

- Click on the plus icon to create a new spreadsheet.

- Title your spreadsheet appropriately, using a specific name such as “April 2024 Budget.”

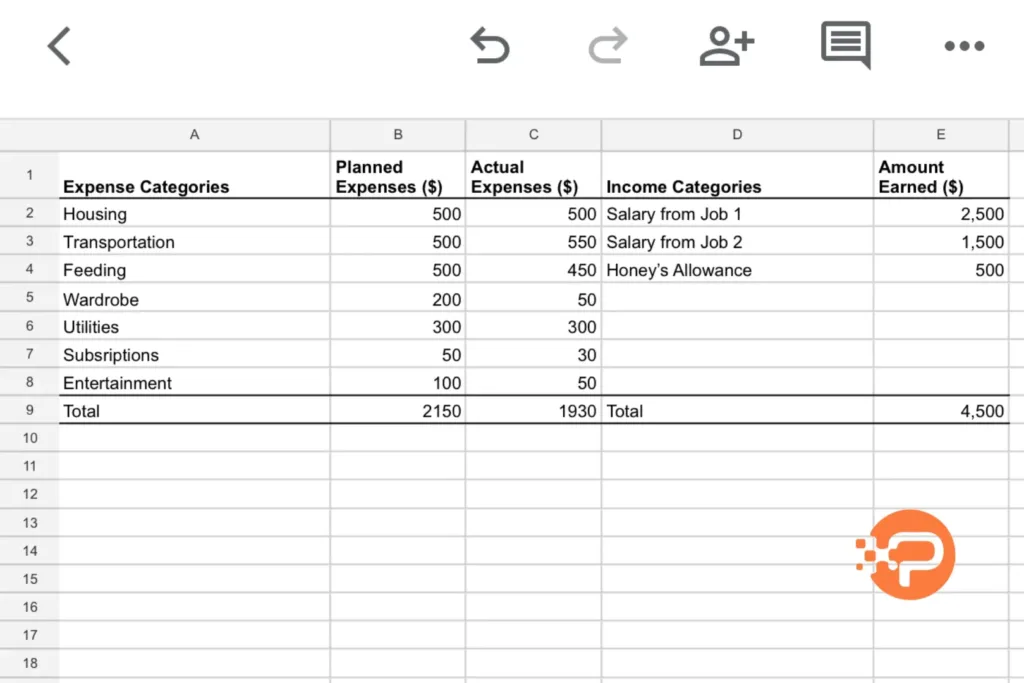

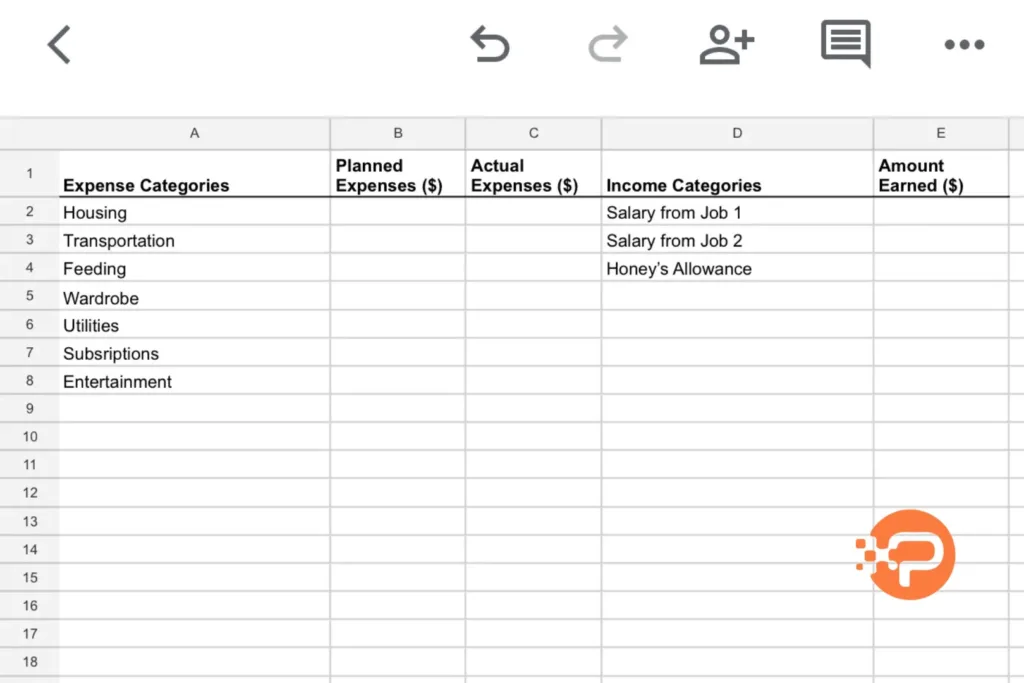

- Create the appropriate column headers for important elements of your budget, such as:

- Column 1: Expense Categories

- Column 2: Planned Expenses (Currency)

- Column 3: Actual Expenses (Currency)

- Column 4: Income Categories

- Column 5: Amount Earned (Currency)

Step 2: Categorize Your Income and Expenses

- Classify all your income and expenses. That is, group your income by source and your expenses by type. For example, if you were a new wife who worked 2 jobs and got an allowance from your husband, you could classify your income as Salary from Job 1, Salary from Job 2 and Honey’s Allowance. On the other hand, you could categorize your expenses into Housing, Transportation, Debt Repayment, Feeding, Utility Bills, Entertainment, etc.

- In column 1 for Expense Categories, write all your categories of expenses.

- In column 4 for Income Categories, write all your types of income. This categorization will help you organize your finances and track where your money is going each month.

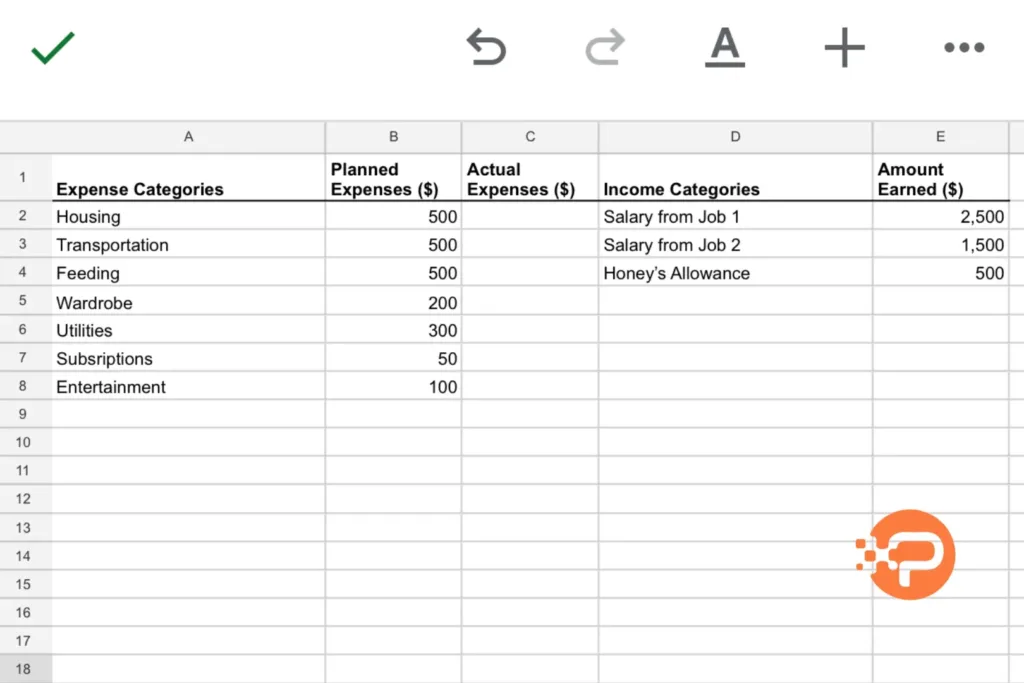

Step 3: Write Your Projected Income & Expenses

- Fill out column 5 for Amount Earned (Currency) with the expected amounts of money you will earn per income category.

- Fill out column 2 for Planned Expenses (Currency) with the estimated amount of money you will spend per expense category. It is important to be both realistic and conservative when estimating your expenses to avoid overspending. To get a more accurate estimate of your monthly expenses, you can review your previous bank statements and consider your typical spending habits.

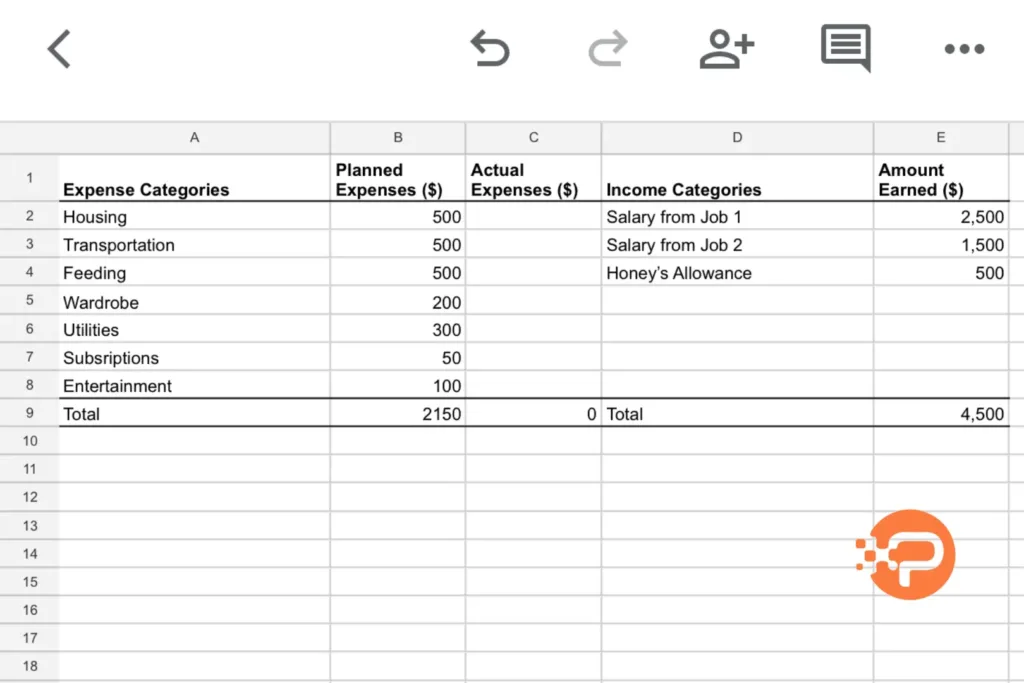

Step 4: Calculate Your Budget Totals

With your income and expenses recorded, the next step is to calculate your budget totals.

- Sum your total estimated expenses at the bottom of the Planned Expenses column using the sum function =SUM(B2:B8).

- Also, sum the total estimated income at the bottom of the Amount Earned column using the sum function =SUM(E2:E8).

- Subtract your total estimated expenses from your total estimated income to determine your disposable income and savings for the month. Ideally, you should have more income than expenses, as this is the first goal of budgeting. But if your expenses exceed your income, you should reevaluate your spending habits and cut back on your expenses.

Step 5: Track Your Expenses

Update the spreadsheet with your actual expenses as they occur throughout the month under the Actual Expenses (Currency) column.

For added convenience, you can also sync your budgeting apps or banking tools with your budget spreadsheet.

Step 6: Review Your Budget

If you review your budget regularly, such as monthly or quarterly, you will discover patterns of spending and opportunities to save better.

Easy peasy, right?

Making a Budget With a Google Sheets Budget Template

Now, let’s learn about the second method of budgeting using Google Sheets.

Making your budget with a Google Sheets Budget Template is simple since you only need to appropriately update the placeholder values. However, it may seem challenging if you edit the cells in the spreadsheet incorrectly.

For example, in a Google Budget template, you should not alter cells that are not highlighted or that include formulas. Also, if you need extra rows, you must copy existing rows in the sheet rather than simply adding new rows; otherwise, the automated functions will not cover the erroneously added rows.

All of this may sound like jargon, but it is quite simple to use. If you can follow these crucial steps and carefully read the instructions and prompts in your spreadsheet, you can use it.

Step 1: Set Up Your Spreadsheet

- In the case that you have not, download Google Sheets from Google Play or App Store.

- Launch Google Sheets and sign up using your email address and password. If you have already signed up, sign in instead.

- If you are using a phone, click the plus icon and select, “New Template.” Then, choose the “Monthly Budget Template.” If you are using a laptop, simply choose the “Monthly Budget Template” from the Google Sheet Template Gallery.

- Title your spreadsheet appropriately, using a title such as “Sample Budget.”

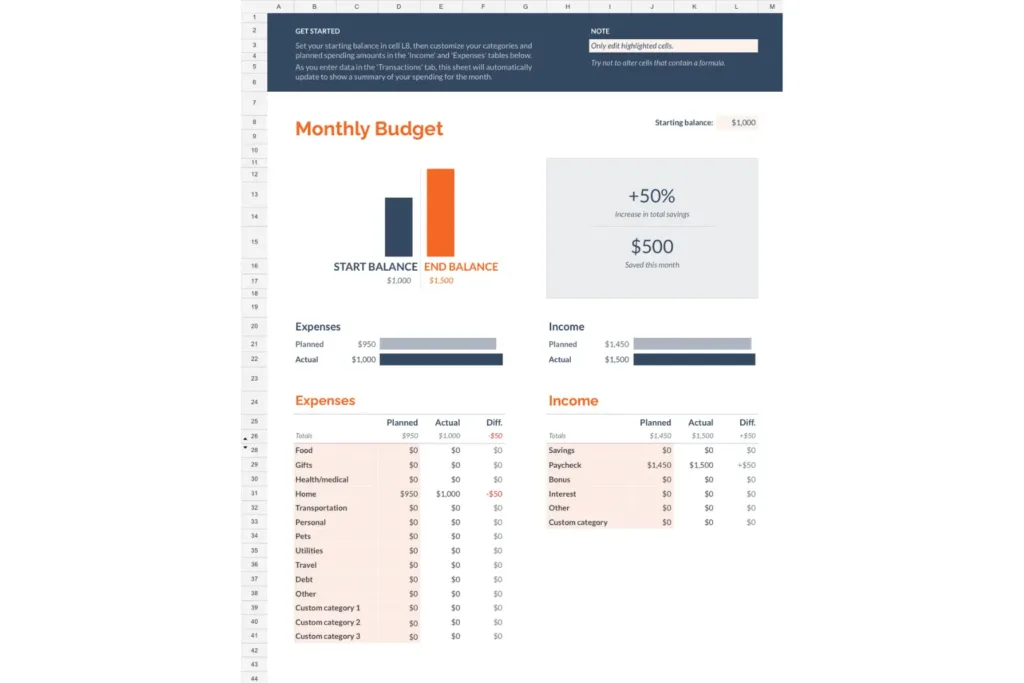

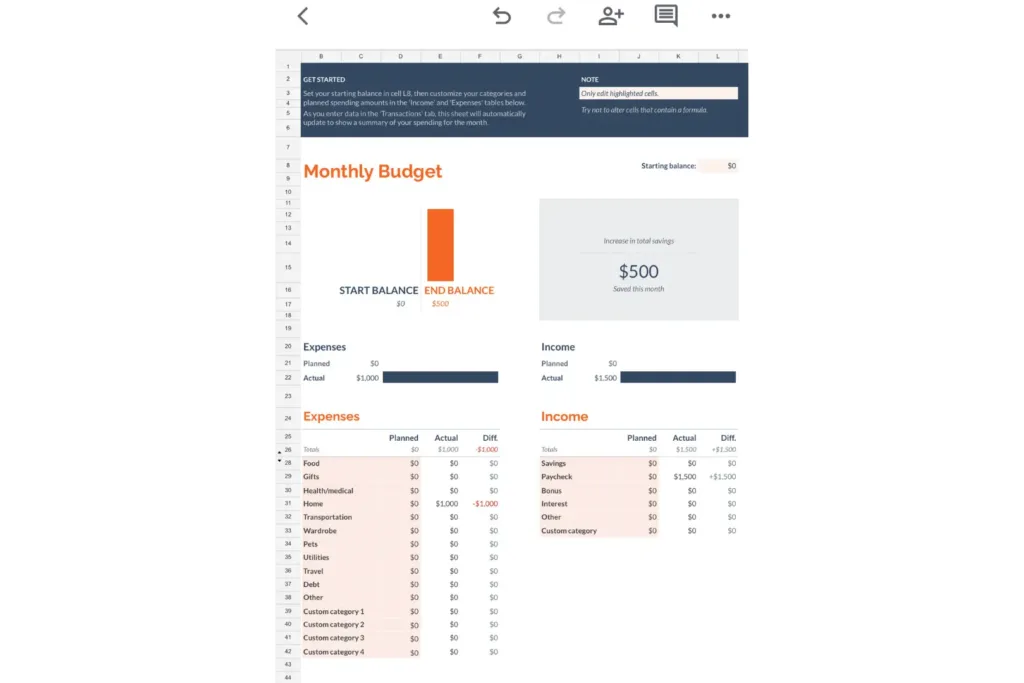

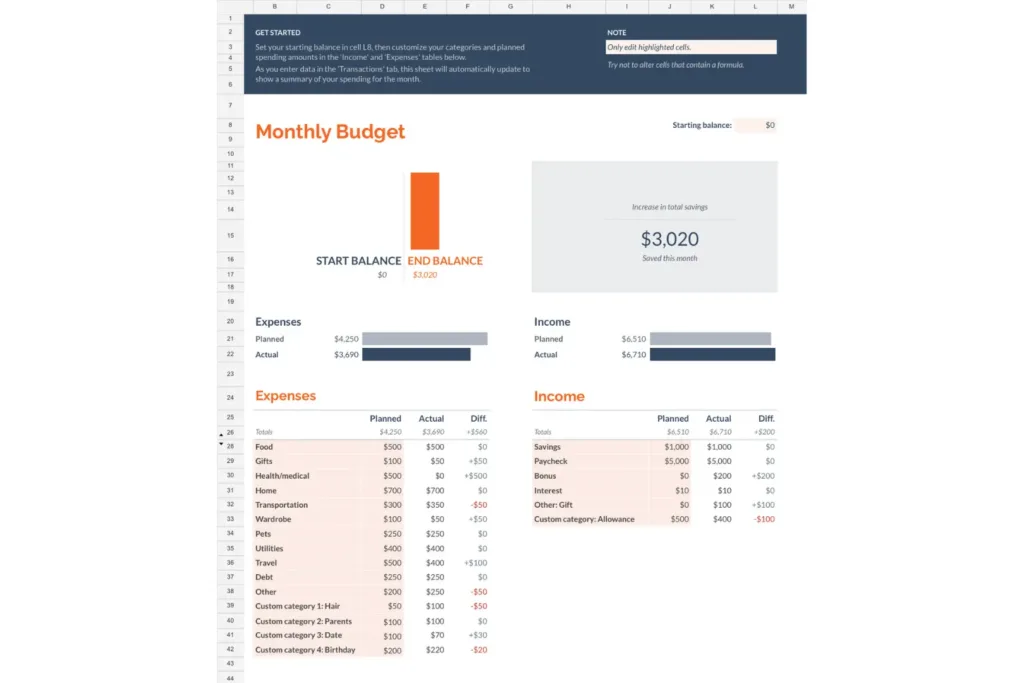

Step 2: Customize the Summary Sheet

The Google Monthly Budget Template spreadsheet contains two sheets: the summary and the transactions sheet. We will first customize the summary sheet. On the summary sheet,

- First, change the starting balance (cell L8), sample home expense (cell D31) and sample paycheck (cell J29) to zero.

- Next, customize the expenses column according to your expenditure. For example, you may change Personal (cell B33) to Wardrobe.

- If you have more expense categories, copy the last row at the bottom (row 41), replicate it for as many rows as you need, and rename the categories accordingly.

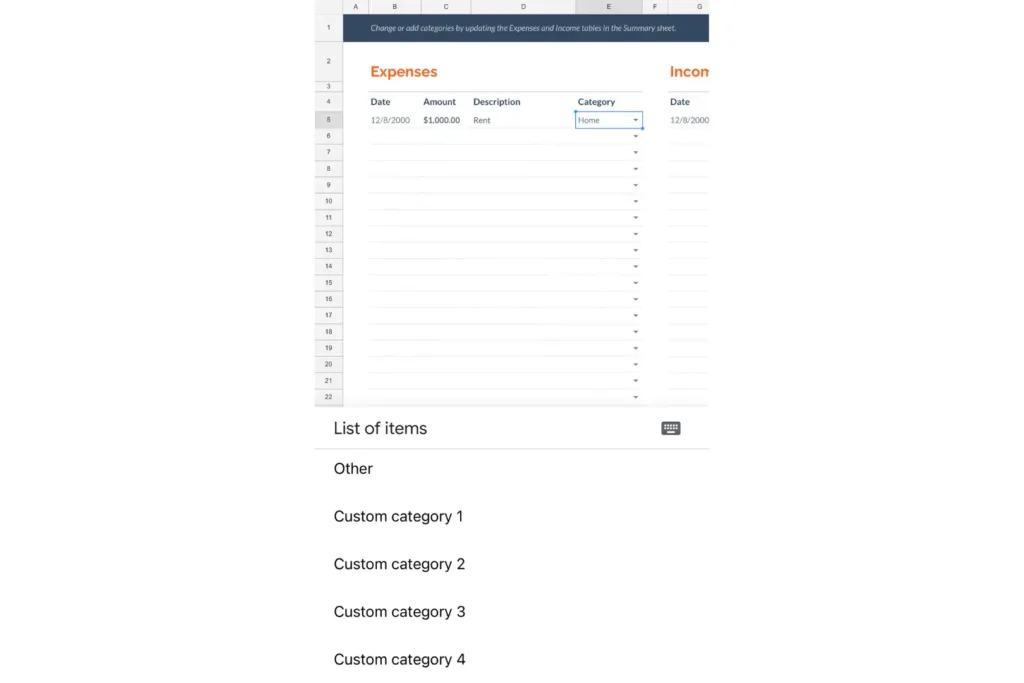

Step 3: Edit the Transactions Spreadsheet

- Open the transactions sheet. You will find sample expenses and income values. Simply delete the values only.

- You may add more rows at the bottom of the sheet since the default transactions sheet contains only 31 rows.

- If you added more categories to your expense categories on the summary sheet, you need to confirm that all the categories reflect on the transactions sheet:

- Highlight the first cell under Category under Expenses (E5) and right-click.

- If all your added categories reflect, skip to step 5. If not, please do not skip.

- Under the Data Menu, select, “Data Validation.”

- Select, “Value contains one from range”

- Click on “Select the data range”

- Change the last two numbers in the data range to match the last two numbers of the cell of the last expense category on your Summary spreadsheet.

- Select, “Done”.

- Confirm that all your categories are reflected in the transactions spreadsheet.

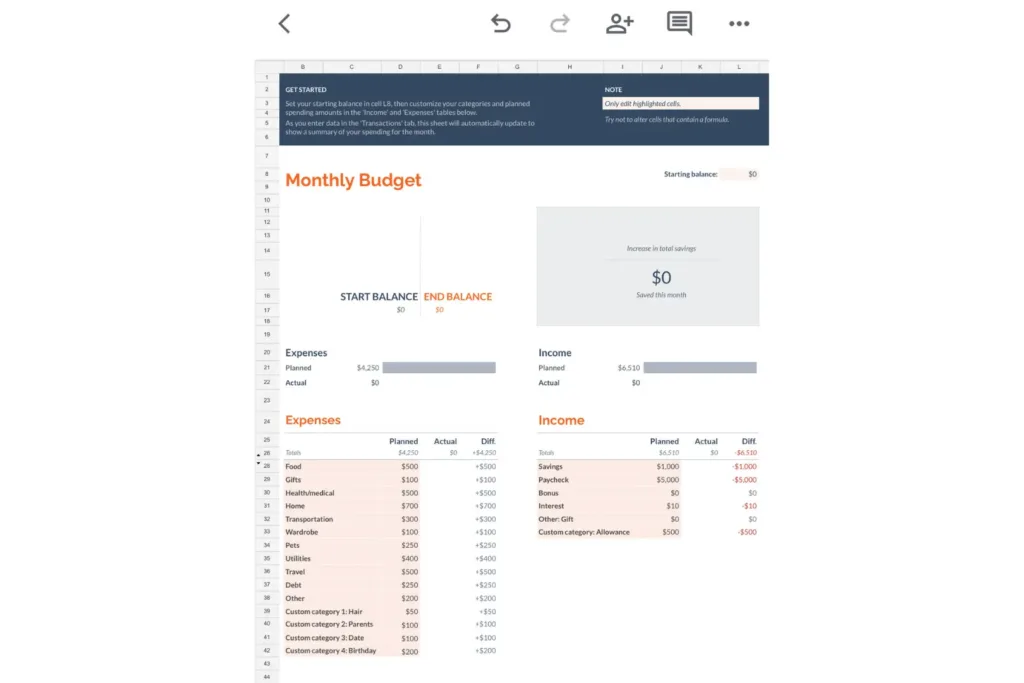

Step 4: Write your Planned Expenses and Planned Income in the Summary Sheet

Record your planned expenses and planned income in the appropriate columns on your summary sheet. Of course, your total expenses should be reviewed if it is higher than your total planned income.

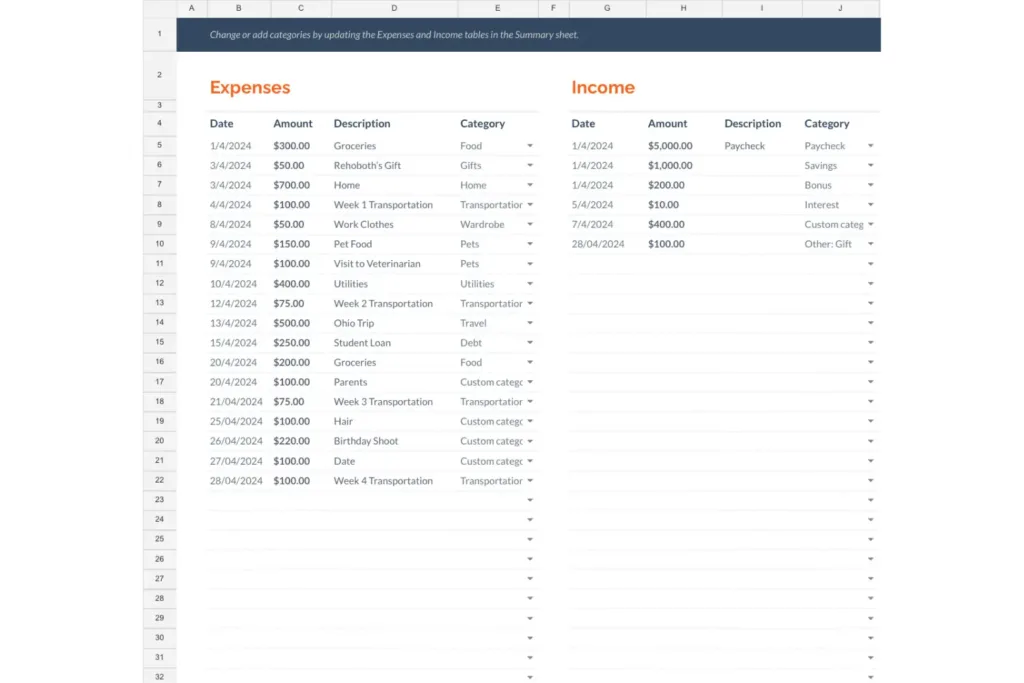

Step 5: Log in All Your Transactions on the Transactions Sheet

When you log in your actual expenses on the transaction sheet and categorize them appropriately, it reflects automatically on the summary sheet. It is important to log in your expenses on the go for accurate documentation of your expenses. Also, a quick glance at your updated summary sheet reveals what quick adjustments you can make to your budget.

Step 6: Track Your Expenses Throughout the Month

On the summary sheet, you will find a clear overview of your:

- Starting balance

- Ending balance

- Planned expenses

- Actual expenses

- Planned income

- Actual income

You can use this information to improve your spending habits, reduce your expenses, and grow your savings and investments.

The Top 10 Free Expense Trackers in 2024

After making a budget, the next financial step to take towards financial freedom is expense tracking. Expense tracking is the meticulous practice of studying and recording how you spend your money, so as to inform your future expenses and savings.

Just like budgeting, expense tracking in 2024 has become easier due to applications called expense trackers. These apps provide ingenious methods of computing, monitoring and curtailing expenses. Although some expense trackers are specifically designed for expense tracking, some personal finance apps or budgeting apps double as expense trackers too.

Now, since these apps provide much financial value, many of them are not free to use. However, after extensive research and comparison of many expense trackers, this section reveals the top 10 free expense trackers in 2024. All 10 apps have paid versions, however, they offer premium expense tracking even in their free versions. Let us dive in!

PocketGuard

PocketGuard is an all-in-one finance management tool that offers expense tracking, budgeting, bill monitoring, savings goals and personalized financial insights.

You can access most of its features without purchasing a premium subscription or making in-app purchases. However, if you require additional functionality, such as automated bill tracking, custom categories, priority assistance, and an ad-free experience, you may need to pay a monthly subscription.

PocketGuard automates the process of tracking expenses by securely syncing with your bank accounts, credit cards and other financial institutions. This eliminates the need for you to manually document your transactions, so you can always have an accurate and up-to-date view of your financial transactions.

However, in comparison to other expense-tracking applications, PocketGuard offers fewer customization options. Also, some customers say the premium features are a bit pricey.

PocketGuard is available for download on both iOS and Android devices at no charge. It has a 3.7 Google Play rating and a 4.6 Apple Store rating.

Goodbudget

Goodbudget is a simple yet powerful budgeting app that digitizes the “old-but-gold” concept of envelope budgeting. With Goodbudget, you create virtual envelopes for various spending categories, allocate funds accordingly, and only spend money from each envelope as needed.

You can track your expenses, make budgets, envelope balances, set savings goals, sync across devices and even share your envelopes with family members.

Goodbudget has a paid version known as Goodbudget Plus, which offers additional benefits, such as an unlimited number of virtual envelopes, automatic syncing with financial accounts, an ad-free experience, priority support and more detailed financial reports. However, its free version is very capable of routine expense tracking and budgeting.

One of Goodbudget’s drawbacks is that the free version does not allow you to connect your bank accounts, so you would have to manually enter your transactions on-the-go. Also, if you compare the app’s user interface to other expense-tracking applications, it is a bit outdated.

Goodbudget is available for download on both iOS and Android devices at no charge. The app has a 4.4 rating on Google Play and a 4.6 rating on AppStore.

Wally

Wally is an intuitive and highly secure personal finance app that offers features for expense tracking, budgeting, goal setting and financial insights.

At its core, Wally simplifies expense tracking by allowing you to manually input transactions or scan your receipts using your phone. Then, it automatically categorizes your expenses and provides basic visual financial reports, which helps you know where your money is going and identify expenses to cut back.

In addition to expense tracking, Wally offers sophisticated budgeting tools that can help you set and track your spending limits for different expense categories.

Wally also allows you to set savings goals for major purchases or specific goals. You can even track your progress towards these goals and receive insights on how to achieve them much faster.

It has a premium version, Wally Gold, which automatically syncs bank accounts, allows for custom expense categories, and provides advanced reports, priority support and an ad-free experience. However, while you cannot enjoy automatic syncing and whatnot on its free version, your expenses are still properly tracked.

Wally is available for download on both iOS and Android devices. The app has a 4.2 rating on the Apple Store and a 2.2 rating on the Google Play Store.

Buxfer

Buxfer is a personal finance management app that offers a range of features to help you track expenses, budget, manage debt and plan for the future. The app has an intuitive interface, tight security and customizable options.

Buxfer simplifies expense tracking by allowing you to manually enter your transactions or automatically sync your financial accounts, including bank accounts, credit cards, and investment accounts, such that you can view all your financial transactions at a glance and understand your spending habits.

This app offers robust budgeting tools that allow you to set spending limits for different categories, track your progress and receive alerts when you approach your budget limits. It even provides you with tools for managing debt and setting up repayment plans.

You would also receive basic reports on income, expenses, assets, liabilities, and net worth to help you make informed decisions about your finances and plan for your bright future.

While the free version of Buxfer offers expense tracking, budgeting and debt management tools, Buxfer Plus, its paid version, provides additional features like automatic bank syncing to unlimited accounts, advanced budgeting tools, enhanced reporting and priority support.

Buxfer is available for download on both iOS and Android devices. It has a 3.5 Google PlayStore rating and a 4.2 rating on the Apple Store.

Honeydue

Couples looking to manage their finances jointly may opt for Honeydue, an intuitive finance app that helps partners track their expenses, make budgets together, set savings goals, repay their debts and stay informed about each other’s financial activities.

Honeydue allows couples to connect their bank, credit card, and other financial accounts to it for free. This allows both couples to view their joint financial activities in one place, giving them a clear picture of their combined spending habits and financial responsibilities.

Honeydue also has features for managing shared expenses, tracking their debts, splitting costs and settling payments seamlessly. It categorizes expenses and flags any disparities or odd expenses by either partner. Financially irresponsible partners are exposed! Lol.

While the free version of Honeydue includes essential features like expense tracking, bill reminders, shared lists, and communication, the paid version, Honeydue Plus, provides additional benefits such as custom categories, advanced bill reminders, transaction search, enhanced security, and priority support.

Honeydue is available for download on both iOS and Android devices. It has a 3.5 Google PlayStore rating and a 4.5 rating on the Apple Store.

Expense IQ

Expense IQ is a user-friendly and all-in-one financial solution for expense tracking, budgeting, debt management and financial analysis. It allows you to manually input your transactions, categorize your expenses and monitor your spending habits over time.

Its stand-out feature is its robust budgeting feature. With Expense IQ, you can make personalized budgets for your different expense categories. The app would send you notifications when you are approaching or exceeding your budget limits, thereby promoting wise spending.

Expense IQ also offers comprehensive debt management features, so you can input and track your debts, such as loans and credit card balances, and set up efficient repayment plans.

It also has a paid version known as Expense IQ Premium. While the free version of Expense IQ offers essential features for expense tracking, budgeting, and debt management, Expense IQ Premium provides additional benefits such as automatic transaction importing, advanced budgeting tools, enhanced debt management features, detailed reports and analytics and priority support.

Expense IQ has a 4.2 Google Play rating. For some reason, it is not available on the Apple Store.

Spendee

Spendee is a user-friendly personal finance app that helps people manage their money efficiently. It has various tools for expense tracking, budgeting and financial analysis, making it easier for users to take control of their finances.

With the free version of Spendee, you can input your transactions manually and see all your expenses in one place. You also can use the app’s budgeting and savings goals tools to plan your finances effectively.

Spendee ensures that all your sensitive information is protected with encryption and security measures, so you can trust the app.

If you want more advanced features, Spendee Premium offers automatic bank syncing to unlimited accounts, advanced budgeting tools, enhanced financial reports and analytics and priority support.

Spendee is available for download on both iOS and Android devices. Spendee has received good ratings from users, with a 4.1 rating on Google PlayStore and a 4.7 rating on the Apple Store.

Toshl Finance

Toshl Finance is a personal finance app that helps you track your expenses, set budgets and analyze your finances. It is user-friendly and offers both manual input of transactions and automatic syncing of bank accounts and credit cards to help you curb their spending and save money.

Additionally, Toshl Finance provides features like bill reminders, currency conversion, financial insights, goal-setting tools, analytics and visualizations to motivate you to achieve your financial goals.

While the free version offers essential features for tracking expenses and basic budgeting, the paid version, Toshl Pro, provides additional benefits like unlimited budgets and categories, advanced budgeting tools, enhanced reporting and insights, and priority support. However, this version is relatively expensive.

Toshl Finance is available for download on both iOS and Android devices. Toshl Finance has really good ratings on both Google PlayStore (4.4) and Apple Store (4.7).

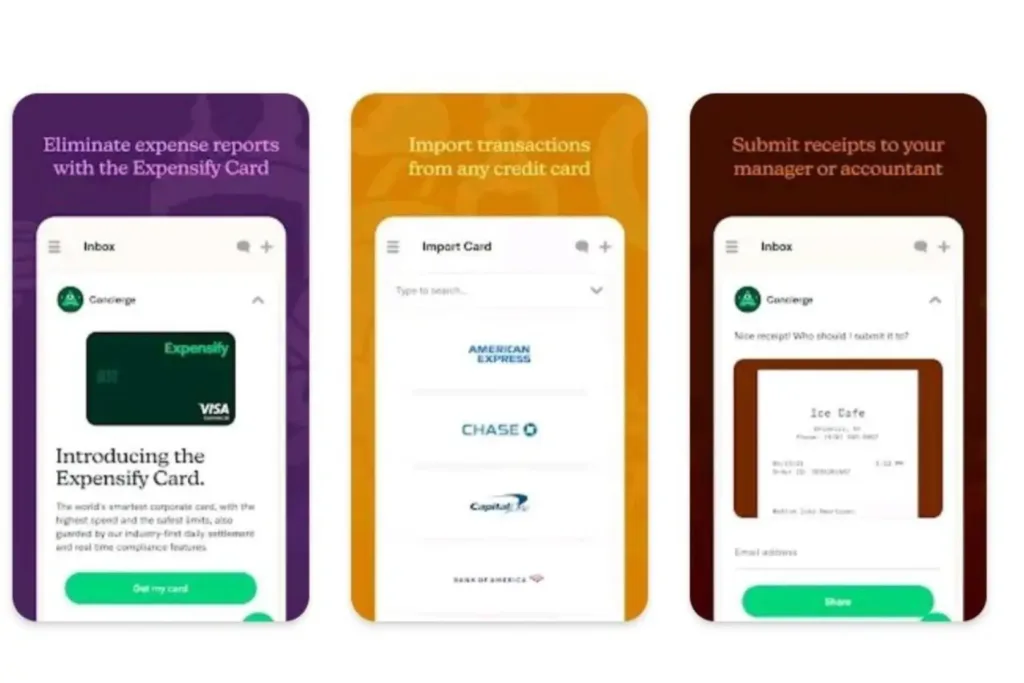

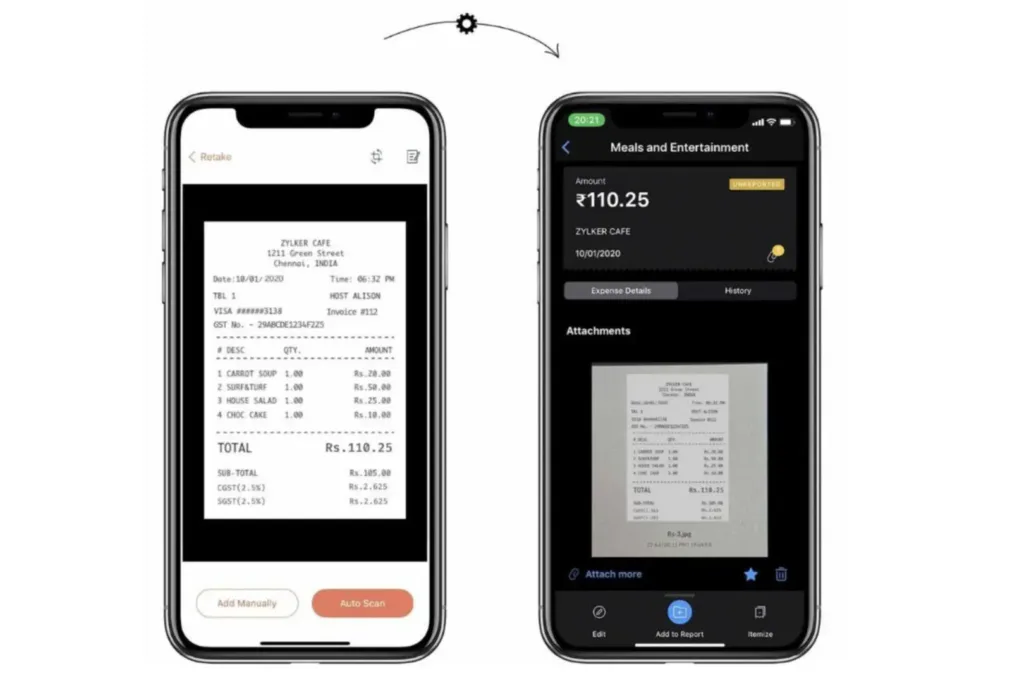

Expensify

Expensify is a comprehensive expense management tool that simplifies the hassle of managing expenses, particularly for businesses and individuals who need to track their spending, organize receipts and streamline expense reporting.

At its core, Expensify is all about tracking expenses efficiently. Whether it’s a takeout, business trip or office supplies, you can effortlessly record their expenses by snapping photos of receipts or manually entering your transaction details.

But Expensify goes beyond expense tracking. It has a slew of features that simplify expense management, such as categorizing expenses, tagging them with relevant information, and assigning them to specific projects or clients.

Expensify also has features designed specifically for businesses and organizations, such as corporate credit card reconciliation and integration with popular accounting software like QuickBooks and Xero. It also simplifies the reimbursement process for employees by offering direct deposit reimbursement.

While the free version of Expensify offers expense tracking and premium reporting features, Expensify Premium provides additional benefits such as automatic receipt scanning, advanced reporting, unlimited integrations, policy enforcement, and priority support.

Notable drawbacks of Expensify include its complex interface and multiple limitations in the free version.

Expensify is available for download on both iOS and Android devices. It has high ratings on both Google Play (4.2) and Apple Store (4.7).

Zoho Expense

Zoho Expense is a user-friendly expense tracking and management software designed to simplify the process of managing business expenses. It has a comprehensive suite of tools that streamline expense reporting, automate reimbursement workflows and provide valuable insights into company spending.

One of the key features of Zoho Expense is its seamless integration with other Zoho applications, such as Zoho Books and Zoho CRM. This integration allows you to sync expense data with other business processes, such as accounting and customer relationship management, creating a cohesive and efficient workflow across the organization.

In addition to expense tracking, Zoho Expense provides powerful analytics and reporting tools that you can use to identify cost-saving opportunities, optimize budgets and make informed financial decisions in your business.

The free version of Zoho Expense offers basic expense tracking and reporting features. However, Zoho Expense Premium provides additional benefits such as automatic expense capture, advanced reporting, enhanced integration options, policy enforcement features and priority user support.

Zoho Expense is available for download on both iOS and Android devices. It has high ratings on both Google Play (4.6) and Apple Store (4.8).

Mint: The Best, or Not?

At the moment, Mint seems to be the people’s favourite because of its user-friendly interface and comprehensive features. With Mint, all of your financial information—bank accounts, credit cards, loans and investments—are conveniently consolidated in one location. Mint presents customizable budgeting tools which allow users to set financial goals and receive alerts when they exceed their spending limits. It also sends bill reminders.

If you are familiar with budgeting apps and expense trackers, you may have wondered why Mint did not come up until now. Well, here is why. Mint has shut down and has been absorbed by Credit Karma. Hence, it is not among the 10 best expense trackers in our books.

Why Not YNAB, Mint’s “Replacement”?

The YNAB app is a comprehensive finance app which takes a proactive approach to budgeting by emphasizing the need to allocate every dollar. It allows users to allocate funds to specific categories, such as groceries, bills and entertainment, thereby promoting mindful spending.

YNAB also provides educational resources and live workshops to help users master budgeting. It also provides robust community support through forums and social media channels which fosters accountability and motivation. Honestly, it is so good that it is often referred to as Mint’s “replacement”.

However, YNAB has two major drawbacks that do not allow us to include it in our list of free expense trackers. After a 31-day trial, it requires a subscription fee which might put off budget-conscious people, although many users argue that the benefits outweigh the cost. It also has a complimentary learning curve that new users may find difficult to follow.

The 15 Best Ways to Save in 2024

The goal of budgeting is financial freedom.

Consistent saving is necessary for anyone who wants to have something to fall back on in hard times or to invest with when opportunities present themselves.

In this section, we will discuss the 15 best ways to save in 2024. We will learn simple and creative ways to ensure that our financial futures are not compromised by the state of the economy. Follow me.

Budgeting

Undoubtedly, the habit of saving starts with creating a budget. By creating a budget, you can gain a clear understanding of your income, which will then inform your expenses and savings.

Budgeting helps you to identify areas where you can reduce your spending and allocate more towards your savings goals, whether it be paying off debt or saving for a major purchase.

Additionally, budgeting promotes accountability and discipline, which helps you stay on track with your financial goals. If you want to save in 2024 regardless, start by creating a budget.

Automate Your Savings

This is undeniably one of the best ways to save in 2024, and here’s why: life can get hectic, and sometimes, our best intentions to save can get lost in the shuffle of daily expenses and distractions.

By setting up automatic transfers from your checking account to your savings account, you’re essentially removing the temptation to spend that money elsewhere. It’s like paying yourself first before your other expenses have a chance to chip away at your savings goals.

Also, automating your savings ensures consistency as you will save the same amount regularly without having to remember to do it manually each time. It is a simple yet powerful strategy that can significantly improve your financial well-being.

Cancel Subscriptions

Subscriptions have a sneaky way of accumulating, and those seemingly small monthly fees can add up to a substantial chunk of your budget. Canceling subscriptions is really about reassessing your priorities and redirecting funds to areas that align more closely with your financial goals.

For example, think about the multiple streaming services you might be subscribed to. Sure, each service may only cost a few dollars a month, but when you’re juggling multiple platforms, it quickly becomes a significant expense.

For instance, canceling one streaming service that costs $10 per month can save you $120 annually. Multiply that by a couple of services, and you’ve got a noteworthy sum that could be better allocated elsewhere. There are also those gym memberships we tend to forget about.

If you’re paying for a gym you rarely visit, consider redirecting that money to home workout equipment or outdoor activities. You’ll be surprised how much you can save while still staying fit and healthy.

In summary, cancelling subscriptions is a simple yet impactful step towards achieving financial freedom in the ever-evolving landscape of personal finance.

Prepare your meals

If you want to save some money, cooking at home is an excellent option. Eating out can quickly lead to an empty wallet while preparing meals at home tends to be more cost-effective.

Besides, home-cooked meals are often healthier since you have more control over the ingredients and cooking methods. To save better in 2024, try planning out your meals in advance, buying groceries in bulk and batch cooking.

Practice Delayed Gratification

In today’s fast-paced world, where everything is available at the click of a button, developing the habit of delaying gratification can have a profound impact on your financial well-being.

It is essential to differentiate between your needs and wants before making a purchase. You could take 24 hours to reflect before making an unplanned purchase. This pause can help you evaluate whether the purchase is necessary or something that can be put off. Often, the desire to buy subsides over time, and you may find that you can save a considerable amount of money by avoiding impulsive purchases.

Smart Shopping

When you’re planning to make a significant purchase, take some time to research and compare market prices. Don’t settle on the first offer you come across. The first price is usually a false price!

Look for discounts and promotions to ensure that you get the best possible value for your money. Additionally, consider purchasing thrift items instead of brand-new ones, as they can often be significantly cheaper and still in great condition. Making these few adjustments can help you save a lot of money in the long run.

Tracking Your Expenses

Imagine going on a 10-hour road trip without Google Maps. You could end up lost or waste time, fuel and money. Similarly, without tracking your expenses, you are essentially navigating your financial journey blindly.

By meticulously recording your purchases, you gain invaluable insight into your spending habits. This clarity allows you to identify areas where you can cut back or make more mindful choices. It’s like shining a light on your finances, revealing opportunities to save that may have otherwise gone unnoticed.

Plus, with the plethora of budgeting apps and tools available today, tracking expenses has never been more convenient. So, if you’re serious about saving money in 2024, consider tracking your expenses a priority.

Paying Off Debts

When you carry debt, you’re not just paying back what you borrowed. Actually, you are also shelling out extra money in the form of interest. High-interest debts, like credit card balances, can eat away at your finances, leaving you with less money to save or invest.

By prioritizing debt repayment, you’re essentially saving yourself from paying unnecessary interest fees, freeing up more of your income for future savings goals. Plus, once you’re debt-free, you can redirect those payments towards building your emergency fund, investing for retirement, or achieving other financial milestones.

So, while it may not seem as flashy as investing in the stock market or saving for a dream vacation, paying off debts is a solid foundation for building a healthier financial future.

Negotiate Your Bills

African mothers are the masters of negotiation. It worked in their time, and it still works! Many open market sellers and service providers, such as internet providers and insurance companies, are often willing to offer discounts or incentives to retain customers.

By taking the initiative to negotiate, you can potentially lower your bills and free up more money to put towards your savings goals. It’s a simple yet effective way to make your hard-earned money last in today’s economy.

Invest

Unlike traditional savings accounts, which typically offer low interest rates that struggle to keep pace with inflation, investing allows your money to work harder for you. By spreading your funds across a range of diverse assets like stocks, bonds, real estate, and commodities, you can reduce risk and increase your chances of earning higher returns in the long run.

What’s more, investing has never been more accessible or cost-effective, thanks to advancements in technology. You can start with small amounts and gradually build your investment portfolio over time.

However, it’s crucial to educate yourself, seek professional advice, and stay up-to-date on market trends before making any investment decisions. This way, you can make informed choices that align with your risk appetite and financial goals.

Building an Emergency Fund

Building an emergency fund is like creating a financial safety net for unexpected expenses or crises that life may throw your way. It involves setting aside a specific amount of money in a readily accessible account, typically equivalent to three to six months’ worth of living expenses.

Unlike regular savings, which are often earmarked for specific goals or purchases, an emergency fund is reserved exclusively for unforeseen circumstances, providing peace of mind and financial stability during challenging times.

You can start by setting a realistic goal for your fund, aiming for at least three to six months’ worth of living expenses. Then, commit to consistently saving a portion of your income each month until you reach that target. Small, regular contributions can add up over time to provide peace of mind when you need it most.

Maximizing Employee Benefits

Maximizing employee benefits isn’t just about understanding what’s offered—it’s about strategically leveraging those offerings to optimize your financial well-being in 2024 and beyond.

Companies commonly provide employees with benefits such as healthcare coverage, retirement plans and professional development opportunities.

With the changing landscape of employment and evolving market trends, companies typically modify their benefit packages to stay competitive. By staying informed about these changes, you can take advantage of new offerings or negotiate for better terms that could result in cost savings or enhanced coverage.

Reviewing Your Banking Options

Have you ever gone through your bank statement only to find ridiculous fees, such as bogus SMS charges, unexplained money losses, coupled with really small interest? If this is true for you, you may need to change banks!

In order to maximize your savings and ensure that your financial goals are being met, it’s important to periodically review your banking options. By so doing, you can minimize fees, maximize interest earnings and take advantage of promotions or incentives offered by banking options that align with your financial goals.

Getting a Side Hustle

Yes, yes, I know getting a good job may be tough, not to talk of a side hustle. But really, it is possible!

Think of your main income as the stream that covers your essential expenses and meets your financial obligations. Then, think of your side hustle as the stream that allows you to save more and enjoy your life.

Whether it is a small business, freelancing, tutoring or selling services online, investing your spare time in a side hustle not only diversifies your income but could be the key to substantial savings in this economy. If you can get one, please do!

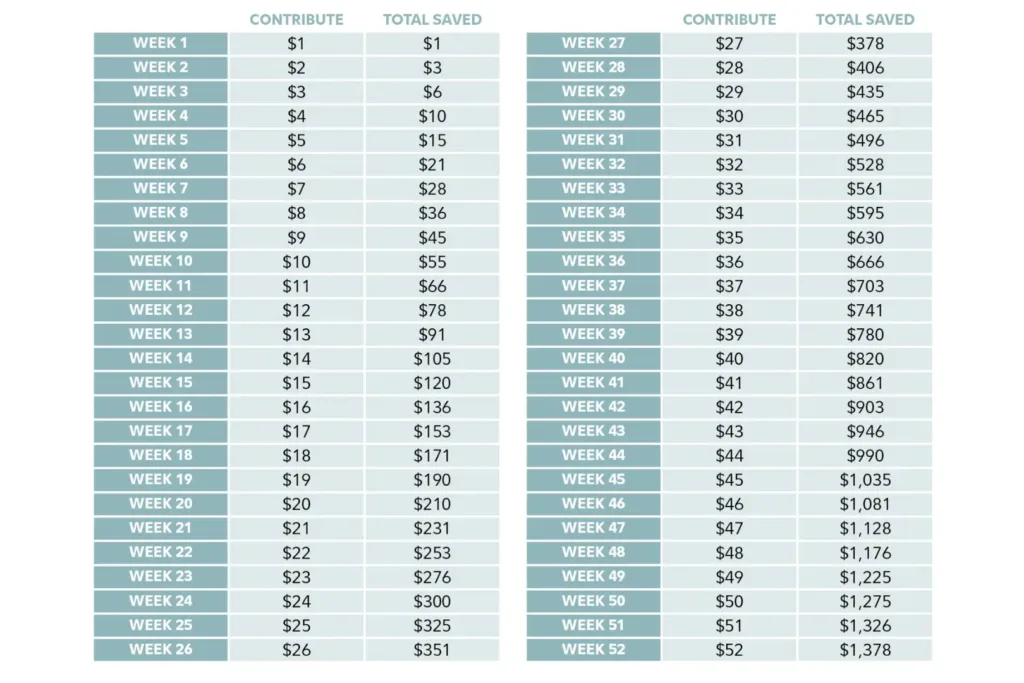

Jump on a Savings Challenge

Jumping on a savings challenge is a great way to save in 2024 because it adds an element of fun and motivation to your saving journey.

For instance, you could jump on the “52-Week Money Challenge,” where you save a specific amount each week corresponding to the week number (e.g., $1 in week 1, $2 in week 2, and so on). By the end of the year, assuming you are faithful to the process, you’ll have saved $1,378.

If you are struggling to save, particularly due to unaccountability, you should jump on a savings challenge!

What Next?

I celebrate you for taking your time to read this guide. This suggests that you are willing to take the bull by the horns in your finances!

Now that you have read this article, what should you do that would justify your investment of time and energy in reading this guide?

First, choose a budgeting method. Second, create your budget. Third, track your expenses daily. Fourth, save towards your financial future. If you can properly implement these 4 steps, your finances will change forever!

Frequently Asked Questions

What are the 7 best free budgeting apps in 2024?

The 7 best free budgeting apps are PocketGuard, Goodbudget, Personal Capital, Every Dollar, Wally, Honeydue and Expense IQ.

What are the 7 best free budgeting apps in 2024 for iOS?

The 7 best free budgeting apps for iOS are PocketGuard, Goodbudget, Personal Capital, Every Dollar, Wally, Honeydue and Expensify.

What are the 7 best free budgeting apps in 2024 for Android?

The 7 best free budgeting apps for Android are PocketGuard, Goodbudget, Personal Capital, Every Dollar, Wally, Honeydue and Expense IQ.

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting method that recommends allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayments.

What is the 50/30/20 rule in Nigeria?

The 50/30/20 rule in Nigeria is the same as it is around the world. Also known as the “balanced money formula,” it recommends allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment.

Does the 50/30/20 rule work?

Yes, the 50/30/20 rule works, especially for budgeting novices with few financial commitments or debts to repay. However, it may not apply for persons with significant financial liabilities, bigger investment risk appetites or peculiar financial needs.

What is the 40/40/20 rule?

The 40/40/20 rule is Grant Cardone’s alternative budgeting ratio, which is better suited for building wealth. It suggests that you should set aside 40% of your income for taxes, 40% for savings, and 20% for needs.

What is the 30-day rule to save money?

The 30-day savings rule recommends that you postpone all your unplanned purchases for 30 days and save the money you intended to spend. This gives you enough time to consider the need for that purchase. If you decide that you need to make the purchase after 30 days, you can go ahead.

What is the 100 envelope challenge?

This is a simple savings challenge in which you number 100 envelopes from 1 to 100. Then, you save the corresponding amount of money in dollars every day for 100 days. By the end of the 100 envelope challenge, you should have saved $5,050.

How much money can you save in 52 weeks?

You can save exactly, more or less than what you plan to save in 52 weeks. However, following the 52-week challenge, where you save a specific amount each week corresponding to the week number (e.g., $1 in week 1, $2 in week 2, and so on), you can save $1,378 in 52 weeks.

What is the best software for tracking expenses?

What you consider to be the best software for tracking expenses depends on your financial needs and inclinations. While some lean towards simple, intuitive expense apps, others prefer comprehensive finance apps. The best apps for tracking expenses include:

- YNAB

- PocketGuard

- Goodbudget

- Wally

- Buxfer

- Honeydue

- Expense IQ

- Toshl Finance

- Expensify

- Zoho Expense

Is there a completely free budget app?

Perhaps, there are completely free budget apps. However, their user ratings may not have positioned them among the top 20 budget apps. The following budget apps offer decent budgeting in their free versions:

- PocketGuard

- Goodbudget

- Wally

- Buxfer

- Honeydue

- Spendee

- Expense IQ

- Toshl Finance

- Expensify

- Zoho Expense

Is there a free budget app that I can use without syncing my bank accounts?

Yes, there is. Goodbudget, Wally, Buxfer and Spendee are examples of free budget apps that you can use without syncing your bank accounts.

What is the best budgeting method?

The best budgeting method is the budgeting strategy that works for you, as certain budgeting methods are more suitable for your current financial phase. Find out which one is more suitable for you here. Feel free to tweak any of the budgeting methods to cater for your lifestyle, needs and goals.

What should I put in my budget?

Basically, your budget should comprise your net income, projected expenses and actual expenses. Your projected expenses should not exceed your income. Also, your actual expenses should not exceed your projected expenses.

What is the best way to budget?

While there are popular and efficient budgeting methods, such as the 50/30/20 rule, zero-based budgeting, envelope budgeting, percentage-based budgeting, and bi-weekly budgeting, the best way to budget is to adopt the budgeting strategy that works for you!

What are the 6 steps to creating a budget?

The 6 steps to creating a budget are:

- Identify all your sources of income.

- Add all your income.

- List your fixed and variable expenses.

- Add your estimated expenses.

- Track your expenses.

- Review your budget.