I assume you are reading this article to learn how to create a personal budget. This suggests that you are ready to take the bull by the horns in your finances. You are in the right place!

However, before we delve into the crux of this article, I would like to define some important terms to help you grasp the concept of budgeting and how to create your budget. Follow me.

What is a Budget?

A budget is a financial plan for your income, expenses, and savings over a specific period, typically monthly. With a budget, you can allocate your income to categories such as housing, transportation, feeding, debt repayment, and so on. This helps you learn how to spend your money wisely and work towards your financial goals.

What is a Personal Budget?

A personal budget is slightly different from a budget. You could call it a type of budget that is customized to your current financial needs, responsibilities, and goals. It takes into consideration your lifestyle and preferences.

So, what sets a budget apart from a personal budget? The main difference lies in the level of customization and personalization. While a budget provides a general framework for managing money, a personal budget tailors that framework to your circumstances.

Why Do You Need to Create a Personal Budget?

Here are some important reasons why you should take time to create a personal budget, even if it seems like a chore.

- Financial Awareness:

Sometimes, your income looks like a whole lot until you sit down to allocate your resources. A personal budget gives you a clear picture of what you earn, what you spend it on, how much you should spend, and what you should save. In a personal budget, your expenses are categorized such that you can see what is taking a chunk of your resources and where you can cut back.

- Wise Spending:

Have you ever been paid your salary at the end of the month, only to spend it all in a week? This should not happen under normal circumstances! A personal budget allows you to allocate your resources towards your expenses, debts, and savings over a period, usually monthly. With a personal budget, you can identify when you are going overboard with your expenses.

A personal budget helps you to be more financially responsible towards those you owe. In a personal budget, you can allocate consistent contributions towards repaying your debts within a stipulated timeframe. You can also determine when to repay more or less.

- Consistent Savings:

Saving a specific percentage of your income every month is a life-changing hack. A personal budget helps you to save consistently towards your financial goals. It also helps you to build an emergency fund for rainy days.

How to Create a Personal Budget

With this step-by-step guide to personal budgeting, you can start almost immediately. Although these steps may require lifestyle changes, you can be confident that they will benefit you in the long run.

Step 1: Know What You Earn

Do you earn a monthly salary? Have you got a side hustle? Does someone give you an allowance? Do you receive compensation at work? Do you receive honoraria? These are important questions to help you identify all the places you get money from. Using a budgeting app, google spreadsheet, or pen and paper, write all your sources of income.

Step 2: Total Your Income

Add everything you make from all your sources of income. Ensure that all statutory deductions have been made. We don’t want any problems with the government, do we?

Step 3: List Your Fixed and Variable Expenses

Your expenses fall into two classes: fixed expenses and variable expenses.

Fixed expenses are expenses that you typically spend the same or similar amount of money to cover monthly, such as housing, subscriptions, student loans, and so on.

On the other hand, variable expenses are expenses that you spend variable amounts of money to cover monthly, such as feeding, clothing, entertainment, and so on.

List your fixed expenses and allocate resources to them. You may look through your bank statements and receipts to get an accurate estimate of the amount you need to budget for every expense.

Next, list your variable expenses and allocate resources to them. It is also important that you do not allocate too much money per expense, so as not to overspend.

Step 4: Total Your Expenses

Add all your expenses.

Compare your total income to the total of your expenses. Your expenses should not exceed your income. You should also have some money to save. If you notice that your expenses are above or slightly below your income, you may need to cut back on your expenses.

A tip for cutting back on your expenses is categorizing your expenses into needs and wants. You should prioritize your needs, such as feeding and housing, above your wants, such as an unnecessary phone upgrade or a new toy.

Step 5: Track Your Expenses

Record all your expenses using a budgeting app, expense tracker, spreadsheet or pen and paper.

If you are using a spreadsheet or pen and paper, it is best to write what you spend just after you spend it to avoid forgetting or mixing things up.

Some free expense trackers and budgeting tools allow you to sync your financial accounts, capture images of receipts, and also manually enter your transactions, so you can track your expenses in one place. Some even send notifications when you overspend. Great, isn’t it? You should try one.

Step 6: Review Your Personal Budget

Personalizing your budget is the essence of creating a personal budget. Your personal budget can change as your goals change.

If your rent increases, for example, adjusting your budget to cater for the increase is a good step to take. You should use your personal budget to stay afloat. So, periodically take a fresh look at it and make adjustments where needed.

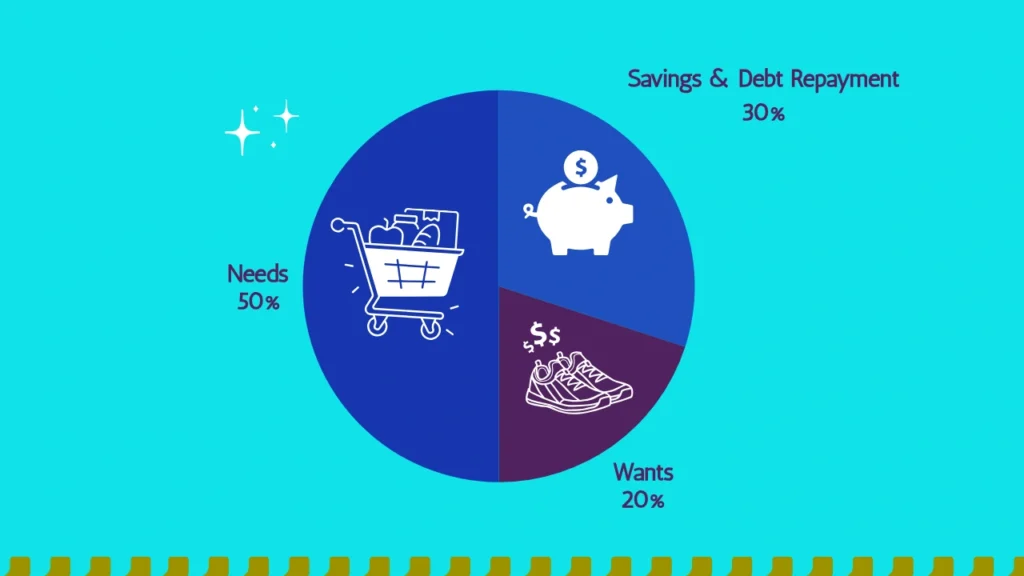

Tweaking the 50/30/20 Rule

The 50/30/20 rule is a popular budgeting method that suggests allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. It has proven to be a simple yet effective method of budgeting.

While this rule is very helpful, especially for beginners in budgeting, it may not be suitable for people who earn low incomes or those who have a lot of debt to repay. This is where a personal budget comes in.

In your personal budget, you can adopt the style of allocating percentages to your expenses, but in different ratios. For example, if you were a first-time salary earner, you could allocate 50% of your income to needs, 30% to savings, 20% to debts, and ignore your wants entirely for a short period.

On the other hand, a retired professor could allocate 30% of his income to his needs, 20% of his income to his wants, and 50% of his income to savings and emergency funds. This is the beauty of a personal budget.

What’s Stopping You From Creating Your Personal Budget?

A personal budget is an excellent tool to help you achieve your financial goals. While you can adopt any popular budgeting method, such as the 50/30/20 rule, following the guide I have shared, you can tweak the method to cater for your lifestyle, needs, and goals. There is no point in following a certain budgeting method to the letter if you cannot achieve your financial goals, right? Now that you know how to create a personal budget, do so today.

Frequently Asked Questions

What is the best budgeting method?

The best budgeting method is the budgeting strategy that works for you, as certain budgeting methods are more suitable for your current financial phase. Find out which one is more suitable for you here. Feel free to tweak any of the budgeting methods to cater to your lifestyle, needs, and goals.

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting method that recommends allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayments.

What should I put in my budget?

Your budget should comprise your net income, projected expenses, and actual expenses. Your projected expenses should not exceed your income, and your actual expenses should not exceed your projected expenses, or else, in each instance, you need to cut back.